Perpetual Markets Economics and Interest Rate Commentary

29 June 2026

Oil prices and tech stock weakness support lower bond yields. US labour market data may weaken this week, continuing the short-term rally.

Key points

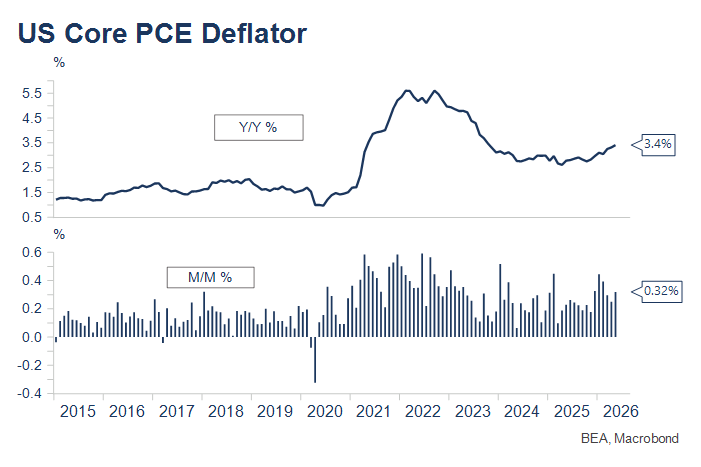

- Lower oil prices and a correction in technology shares contributed to reduced pricing of US interest rate rises, even as PCE inflation continued to track in the wrong direction.

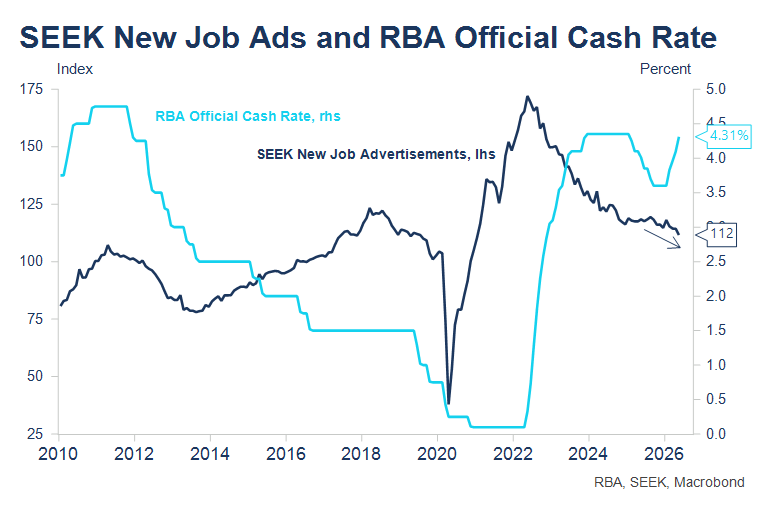

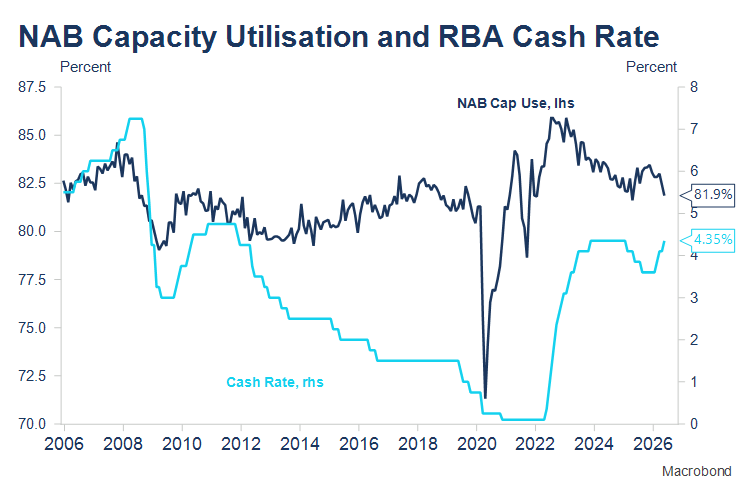

- Australian interest rate pricing of further interest rate rises also reduced and market pricing firms for the next move in interest rates being a cut, though not for quite some time, with only a 50% chance of a cut priced by November 2027. Job ads and cap use are beginning to shift in this direction. It will be important to see if those trends are sustained in coming months given lower oil prices.

- There’s a lot going on in interest rate markets as lower oil prices and technology shares move supportively, even as the Fed signals a more aggressive stance against inflation. This week the focus is all about US labour market data, with both the NFIB and ISM employment intentions series suggesting payrolls could soften more than expectations. That could extend the bond rally in the short-term, however given it was the rise in oil prices that interrupted favourable US labour market developments, the drop in oil prices should reverse this effect in coming months.

- It’s very quiet data wise in Australia this week, with the key event being the RBA Minutes on Tuesday. The market will study the words of the RBA closely to gauge the strength of the RBA’s bias to tighten further. The fact the RBA sees a slowing in the economy as being required to return inflation to target suggests less concern from the Bank about easing house prices and a very small chance of any early return to easing thoughts.

Review of key developments in the past week

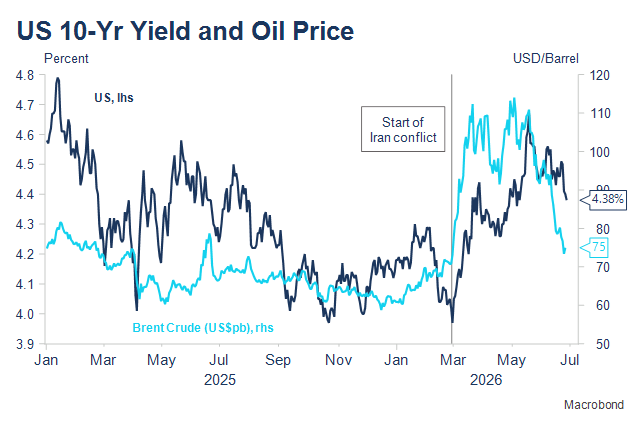

A further drop in oil prices combined with a significant correction in technology stocks - after a blistering rise since April - saw the US market pare expectations of interest rate tightening over the past week even as core PCE inflation remained materially above the Fed’s target and clearly headed slowly in the wrong direction.

The preceding paragraph - and the first three charts - remind that there are some significant, and at times conflicting, pressures impacting the outlook for US (and relatedly Australian) interest rates at the present time:

- Oil prices have been very important since the end of February, both on the upside and downside. Much of this source of inflationary impulse in Australia and the US should unwind over coming months, probably more than the RBA expects.

- Tech stocks have been important in supporting the broader growth outlook but are also adding to inflationary pressure as the AI investment boom rolls on. Apple announced price rises for iPads and Macs last week due to the surging price of chips. Technology has typically been a deflationary influence on global CPIs.

- The pricing of a more hawkish US Federal Reserve has mostly persisted even as oil prices have unwound, though the tech sell off has seen a reduction in the tightening priced over the past week. US markets last week were pricing almost two 25bps interest rate increases by the March 2027 meeting, whereas now peak pricing has just under one and a half rate rises. And while the first interest rate rise was almost fully priced by the September meeting, that has now slipped six weeks to being almost fully priced by the October 2026 meeting. There is still one rate rise priced before the end of the year.

The week ahead – US labour market data and Australian RBA Board Minutes key

In a shortened US trading week due to Friday’s Independence Day holiday, labour market data looms large. Weakness in the US labour market had previously been keeping some Fed officials biased towards further lowering interest rates, though that inclination has more recently been removed by stronger employment growth and continuing low unemployment as well as stronger PCE deflator trends.

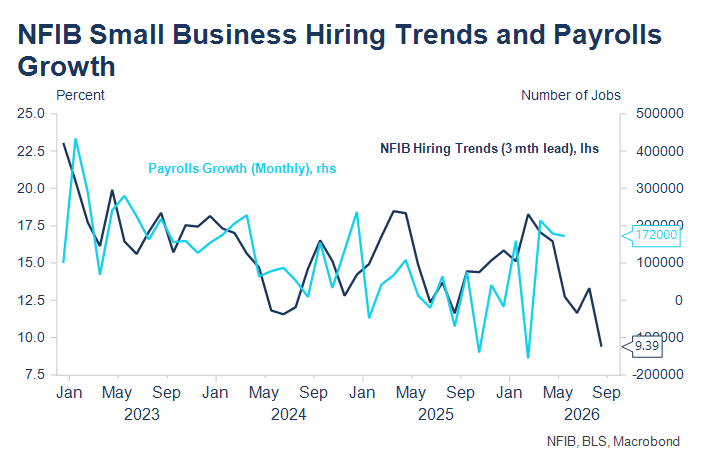

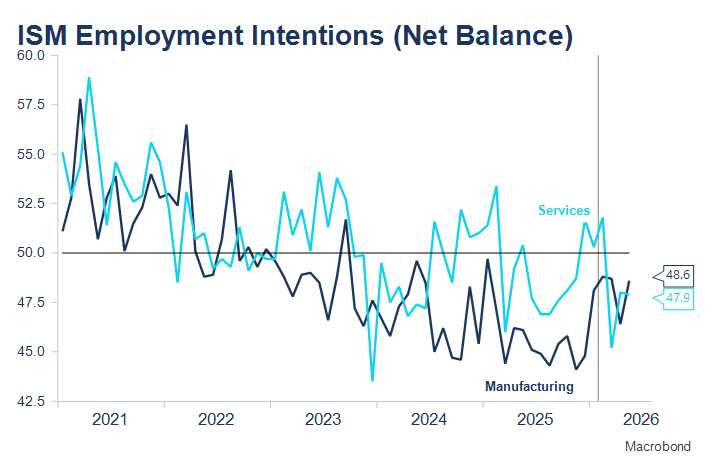

Could this week see that run of stronger payrolls data end? The NFIB series has been a reasonable indicator of changes in the pace of payrolls employment growth and suggests softer numbers could be in evidence as early as this month (last month it still suggested stronger growth), while the ISM employment series, particularly for services, have also moderated. That likely supports an expectation of no more than two interest rate rises in the US, but of course the renewed decline in oil prices should stabilise and potentially reverse those weaker employment signals in coming months. The ISM chart shows the promising improvement in US hiring intentions that was halted by higher oil prices since February.

In Australia, it’s an incredibly light data week, with only the volatile Building Approvals release of interest, leaving focus on the RBA June Board Meeting Minutes on Tuesday and a tantalisingly titled speech by Assistant Governor Kent at 9.30am today: “Additional Monetary Tools: Reflections and a New Framework”. The RBA has published a deal of material reviewing its non-conventional monetary actions during the COVID pandemic. The “New Framework” seems new but doesn’t seem likely to be used any time soon, thankfully.

That will leave focus on assessing the strength of the RBA’s tightening bias, reinforced in the June Decision and the Governor’s press conference. Accompanying statements also noted that the economy needed to slow to return inflation to target, suggesting no early reaction to softer housing prices. Developments over the past week included the expected improvement in unemployment, though employment was revised sharply lower in April, and a reminder from the RBA Deputy Governor that inflation remained “far too high”. Both suggest that Australian markets should continue to price some risk of further tightening in the near term.

Monday 29 June: 9.30am AEST RBA Assistant Governor Chris Kent: “Additional Monetary Tools: Reflections and a New Framework”.

Tuesday 30 June: RBA June Board Minutes. End of Financial Year Australia. Midnight AEST JOLTs, (May).

Wednesday 1 July: Building Approvals (May) (expected unchanged, previous -3.4%, risk stronger). 7.30pm AEST Challenger Job Cuts; Midnight ISM Manufacturing (both the index and prices paid are expected to improve modestly - prices are likely to moderate in coming months given lower oil prices. It will be important to see the extent to which activity and particularly employment indicators recover as this occurs).

Thursday 2 July: 10.30PM AEST Non-farm payrolls, June (+115K jobs growth after +172K in May – risk downside; Unemployment expected unchanged at 4.3%, risk upside).

Friday 3 July: RBA tenders $700m 1.5% 2031.

Continuing the trend seen so far since Chair Warsh took over, there are very few Fed speakers scheduled. Warsh appears on an ECB panel with Lagarde, Bailey and Macklem on Wednesday, while Governor Daly is scheduled on Thursday.

Australian interest rate market developments

Over the past week, Australian interest rate markets continued to reduce the probability attached to further tightening by the RBA and continued increasing pricing, suggesting that the next move in interest rates would be a cut but not until late next year. At present, there is a 50% chance of a 25bps rate cut priced by the November 2027 meeting, exceeding the 37% chance attributed of a further rate increase by the end of 2026.

The level and trend for job ads and capacity utilisation have generally been reliable indicators over time of the trend for Australian official cash rates. In recent months, both indicators have shifted moderately lower, providing a tentative indication that the next move in Australian cash rates might be lower as three of the four major Australian banks now forecast, though not until next year. The jury remains out on the extent to which both indicators might recover as a result of the recent falls in oil prices, though the RBA’s three rate rises likely provide a more enduring headwind.