Perpetual Markets Economics and Interest Rate Commentary

22 June 2026

Fed makes hawkish shift. July meeting live for a US interest rate rise. Australian labour market to unwind much of April weakness. Peace agreement and negotiations remain very fragile.

Key points

- There were two major developments in the past week: the peace agreement between the US and Iran, and a hawkish shift at incoming Fed Chair Warsh’s first press conference.

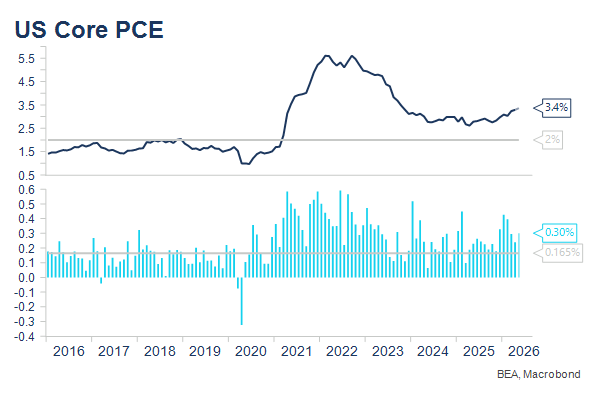

- The peace agreement, provided it holds and the Strait of Hormuz remains mostly open, should see much of the recent spike in inflationary reverse and the stronger global growth picture associated with the AI investment boom re-established. The latter should produce longer, slower inflationary pressures, resulting in further upside for US and Australian short-term interest rates over time. The Fed might well increase interest rates as early as the next meeting if PCE data to be published on Thursday remains elevated. PCE inflation remains elevated and continues to drift higher not lower.

- Warsh’s message seemed clear – the Fed has missed on the inflation part of its dual mandate for the past five years and will deliver prices stability going forward. Out is forward guidance, with a task force to examine Fed communications and the Chair electing not to submit an interest rate forecast. Of the eighteen FOMC members submitting “dots”, nine now see between one and three interest rate rises before the end of the year, compared to twelve that forecast one to four rate cuts as recently as March!

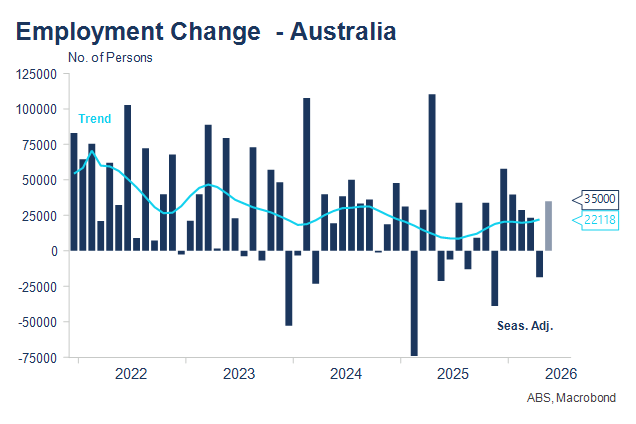

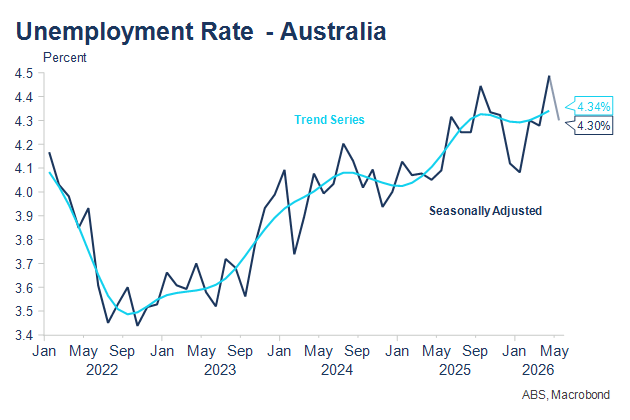

- The RBA left rates unchanged in June and did not consider an interest rate increase. The Board was also clear that it would not hesitate to raise interest rates again if that was required to return inflation to target. This week’s labour market data is important as it was the weaker than expected April data that sparked the initial reassessment of Australian monetary policy forecasts, though the budget tax changes and housing market weakness have built on that foundation. The risk is of stronger than expected employment growth and lower unemployment as the April calendar quirk unwinds. Medium term, my base case remains of a long slow tightening cycle in both Australia and the US as the AI investment boom supports growth, but pressures aspects of the CPI globally.

Review of key developments in the past week

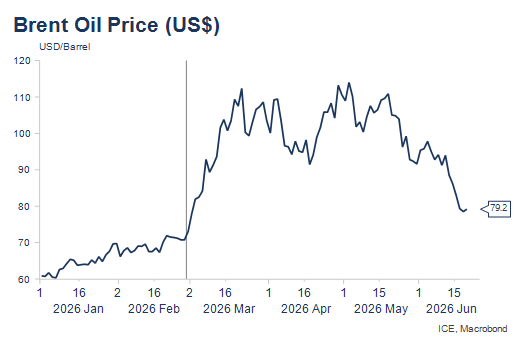

Oil prices fell sharply after confirmation that the US and Iran had agreed to terms of a peace agreement. Prices closed the week around US$9pb or 11% lower than last Friday. That’s only around US$10pb higher than immediately before the conflict began, though pries had increased around US$10pb over January as US warship capacity increased in the Gulf. Over the weekend, prices have risen nearly 2% or US$1.50pb as fighting continues between Israel and Hezbollah in Lebanon, in contradiction of the terms of the peace agreement. Iran has reportedly declared the Strait of Hormuz closed again, though peace talks reportedly continue in Switzerland. This again reminds that Israel is an important third actor in the current conflict. The potential outcomes remain unchanged. A very extended Strait of Hormuz closure will be quite negative for oil prices and growth (but may end at short notice), while provided oil prices can remain around US$70-80pb (or lower), it is likely that the favourable economic conditions for US growth driven by the AI investment boom can be re-established.

The FOMC held its first meeting under new Chair, Kevin Warsh. This saw a very significant shift in US short-term interest rate expectations as Warsh delivered a hawkish message declaring that the Fed will deliver prices stability after having missed on this part of its dual mandate for the past five years. Nine of the nineteen members of the FOMC predicted that there would now be one to three interest rate rises before the end of 2026, compared to twelve members expecting one to four interest rate cuts three months ago! In keeping with Warsh’s views expressed prior to his appointment, the FOMC Statement, Summary of Economic Projections and Press Conference contained far less information than under Chair Powell, with Warsh declining to include his projections for interest rates going forward. The new Chair believes that the signals of markets are important and there is little value in markets merely reflecting what the Fed is saying! Warsh also announced the formation of five task forces to examine: (i) The Fed’s Communications policies; (ii) Inflation measurement and progress toward target; (iii) Balance sheet size and strategy; (iv) Data measurement; and (v) Productivity and labour market functioning (effectively the impact of AI). The Chair described AI as the most important development in his adult life. My view remains that AI is inflationary in the short-term but could well have significant negative impacts on employment over the longer-term.

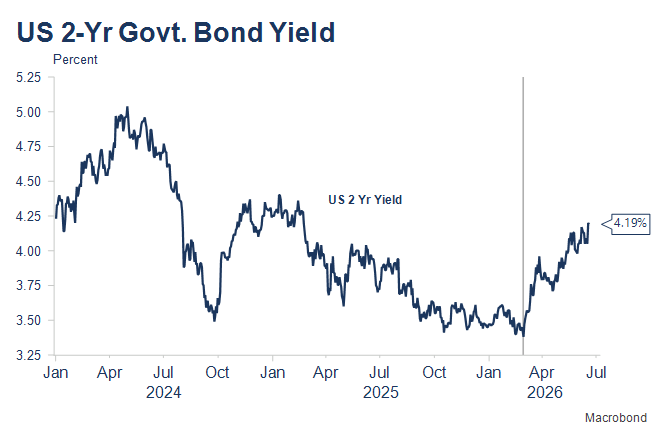

These developments saw US 2-year yields rise 14bps over the week and markets shift the pricing of expected Fed tightening noticeably earlier. Last week, a full interest rate rise was not priced until the first meeting in 2027, and peak pricing was for one and a third rate rises. Now, a rate rise is almost fully priced (96%) by the 16 September meeting (34% probability last week), with peak pricing of nearly two rate increases by the March 2027 meeting. US 2-year interest rates have remained elevated even though oil prices have substantially reversed their recent rise, reflecting the markets’ reassessment of Fed policy, US economic growth and inflation prospects.

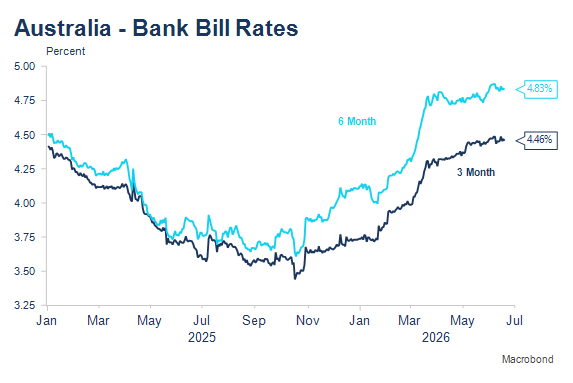

The June RBA Board Meeting saw Australian interest rates remain on hold as universally expected. While the Governor confirmed in the post-meeting press conference that the Board did not consider raising interest rates in June, the Statement saw the addition of words to the effect that the Board would consider raising interest rates further if inflation did not moderate, a sentiment that was mentioned three times by the Governor in the subsequent press conference. Australian short end yields were influenced only slightly by the US rate repricing, with markets now pricing a 60% chance of a further rate rise by the 8 December Board Meeting. Interestingly, however, the market increased the probability it attached to a rate decrease by the end of 2027, from 8% last week to 25% this week. This is the scenario of three of the four major Australian banks, however, there is more diversity in the outlook for Australian interest rates than normal. My base case remains of an elongated (continuing slow) tightening cycle in Australia.

Over the weekend, the Australian government announced that the fuel excise reduction introduced to moderate the influence of the Iran conflict, would be halved from 1 July (to 16 cents per litre). This will likely have limited impact on fuel prices overall given the recent falls in oil prices. The subsidy has clearly worked very well in moderating the short-term impact of the Iran crisis on Australian inflation, despite the protests of many economists.

The week ahead; key Australian and US events

It’s a big week for Australian data with the CPI, Labour Market, Household Spending and Job Vacancies all released, while in the US the focus will be very much on the PCE deflator considering the Fed’s hawkish shift. In light of the latter, and the new Chair’s preference not to guide the market, it will be interesting to see how upcoming speeches differ from the Powell Fed, with governors Waller and Williams’ appearances this week of particular interest. The RBA Deputy Governor delivers the Sir Douglas Copland lecture on Wednesday afternoon, while the Governor participates in a panel in Switzerland next Sunday evening at 10.15pm AEST.

There will be very keen interest in the extent to which employment and unemployment bounce back from the surprisingly weak readings of April. This seems very likely to me, given the unusual calendar quirks of April, with even larger improvements than the market expectation, the risk. The Australian three-year yield rallied ten basis points on the publication of the April labour force data and could retrace somewhat, though the budget tax changes and weakness in the housing market are also playing a role. Housing auction clearance rates remained very low over the weekend.

The monthly CPI is the other important Australian release this week and may provide some indication as to whether there is early price pass through of higher energy prices into broader goods pricing. I think that argument is less relevant given the peace agreement between the US and Iran, which should see much of these inflationary effects reverse as oil markets normalise over coming months. That of course assumes that the peace agreement holds and the Strait of Hormuz remains open; something that has already been challenged by Israeli actions in Lebanon. The key question for markets with respect to Australian monetary policy is whether the three interest rate increases enacted between February and May will be sufficient to return Australian inflation to target. Developments in AI investment and related technology and commodity prices along with the recent much higher than expected National Wage Case decision suggests the risk remains that the RBA is not yet finished, though the peace agreement and housing market softness suggests the Bank can continue to observe the economy for some months. I pencil in the next rate rise in November.

Monday 22 June: 11pm AEST Governor Waller speaks.

Tuesday 23 June: RBA tenders $1bn 4.25% 2036 bonds.

Wednesday 24 June: CPI (May). Trimmed mean 0.3% m/m and 3.5% expected, versus 0.3%/3.4% (April). Headline CPI should fall m/m (-0.4% expected as oil prices fell 15% in the month) but remain elevated at 4.3% y/y. Travel prices are a wildcard, with airlines announcing sales as travel demand declined, but prices for re-routings to Europe surging. 4.30pm AEST RBA Deputy Governor Hauser delivers Sir Douglas Copland lecture.

Thursday 25 June:

- Labour Force (May). Employment expected +30K; Unemployment 4.4%, versus -18.6K and 4.5% (April). Risk stronger employment and lower unemployment as seasonal blip in April due to Easter and school holidays reverses.

- Household Spending (May). +0.5% m/m and +4.2% median forecast compared to -1.1% m/m/+4.5% y/y (April). Petrol prices fell in May, which will be a drag. There’s also uncertainty again about the influence of travel refunds, which were a significant factor in last month’s drop. While there was no doubt further refund activity, Australians have also spent more on indirect routings to Europe suggesting this factor should reverse. I’ll again be looking at an ex-food, ex-petrol and ex-travel measure to try and ascertain the underlying spending trend. UK retail sales were strong in May after a weak April print – the two series are surprisingly often correlated.

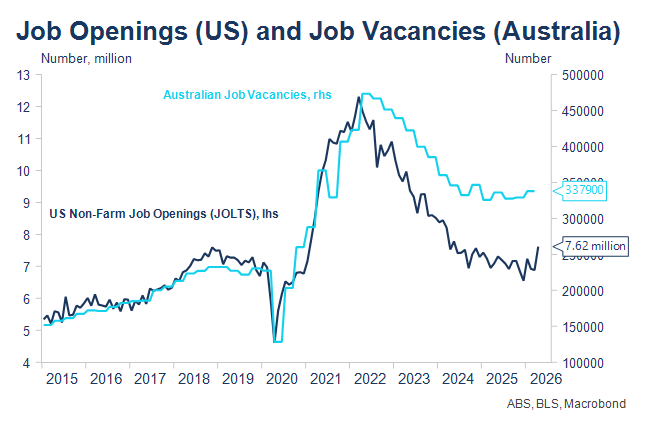

- Job Vacancies (May). SEEK job ads fell around 2.7% in May, perhaps suggesting a softening in labour demand due to the poorly received budget and ongoing elevated fuel pricing and uncertainty from the Middle East. The Statistician’s survey of job vacancies will provide a guide as to the impact of the Iran conflict as it covers the period February to May.

- (Overnight) US PCE deflator (May). This is the key US indicator for the week considering the more hawkish message from last week’s FOMC meeting. Market forecasts expect a 0.3% m/m and 3.4% y/y outcome, up from 0.2% m/m and 3.3% in April. My contention remains that there was evidence of some uptick in US inflation even before the Iran conflict, in part related to the AI boom, and that will justify the moderate tightening in US interest rates now priced over the next six months. As in Australia, inflation remains above target and currently is drifting higher rather than lower. This suggests the risk that the Fed moves rates higher at its next meeting.

Friday 26 June: Three Fed speeches: Williams (5.40am AEST), Goolsbee (8.30am AEST), Kashkari (1.30pm AEST). Socceroos versus Paraguay 1pm!

Sunday 28 June: RBA Governor panel participation in Switzerland (10.15pm AEST).