Perpetual Markets Economics and Interest Rate Commentary – 25 May 2026

Peace deal reportedly close, which should support bond markets in the near-term before short to medium-term bearish trend re-emerges reflecting AI boom.

Key points

- Reports over the weekend suggest an agreement between the US and Iran to end fighting and reopen the Strait of Hormuz is close. If true, after a period of oil market normalisation lasting several months, that should be supportive for bond markets near-term and I’d expect the previous economic outlook to re-establish. That outlook included a continuation of strong AI investment spending and the emergence of inflationary pressures even ahead of the Iran conflict that likely signal a medium-term bearish trend for US bond markets.

- My base case is a long, slow tightening cycle, akin to the mid-2000s’ US housing and Australian mining boom, with Australia benefiting from elevated pricing for gold, silver, copper and lithium. The Fed (and US market pricing) is unlikely to return to easing, though beyond two years I retain concerns about the impact of AI on US employment and inflation.

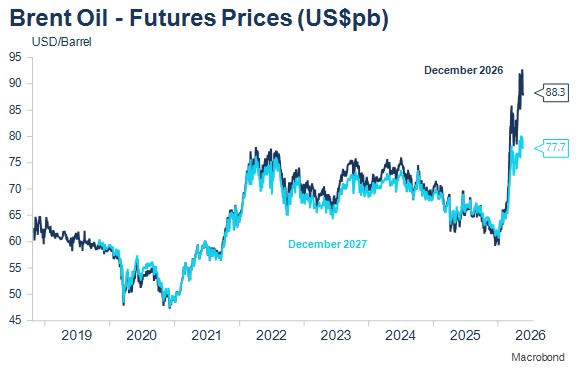

- A peace deal will remove much of the focus on near-term economic data, including on the April CPI and Household Spending Indicator in Australia and April PCE in the US this week. I’d expect the focus to be on Strait of Hormuz shipping movements as this will determine how quickly oil markets can normalise. December 2026 and 2027 futures markets remain near conflict highs suggesting markets expect a slow normalisation.

- A speech this week from RBA Monetary Policy Board member Carolyn Hewson in Adelaide on Wednesday evening and appearances from at least thirteen Federal Reserve members could well be more interesting as the data is again trumped by conflict developments (positive this time). There’ll be interest in the RBNZ’s revised interest rate track on Wednesday; SEEK job ads have been signalling a slow upturn in the NZ labour market.

- A 0.4% or higher core CPI for April in Australia would suggest faster oil price pass through is occurring. That’s a risk, but different to the RBA’s recently released research focusing on the COVID experience, I’m expecting this pass through to be temporary and reversed as oil prices normalise.

Middle East developments

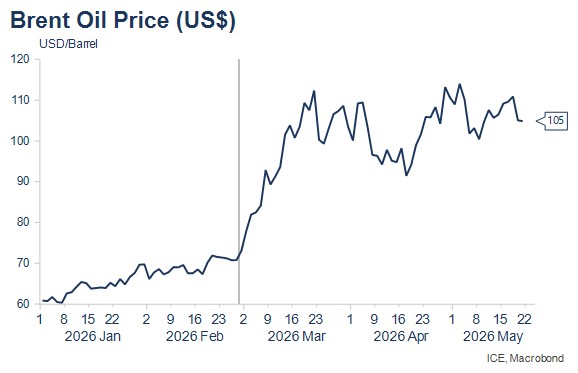

While there were few significant changes to oil prices over the past week, and still a very minimal number of ship transits of the Strait of Hormuz, comments emerging from both President Trump and Iran over the weekend suggest an agreement to end the war and reopen the Strait of Hormuz is very close. More details are expected “in the next few hours” according to US Secretary of State, Marco Rubio.

This suggests it could be a lively start to the trading week in the Asian time zone. Most focus should be on how quickly ship transits in the Strait of Hormuz return to pre-conflict levels. This, along with the extent of damage to infrastructure and how quickly this can be repaired, will in turn determine how quickly oil prices might normalise reducing medium-term inflation concerns. December 2026 and 2027 futures prices on Friday remained near the highs traded since the conflict began but should pullback this week if a deal has indeed been reached to reopen the Strait. Weekend oil markets on IG Markets show only a 4% or US$3.80 drop in the spot oil price suggesting markets are expecting a slowish recovery in oil markets.

![]()

Interest rate market developments and pricing

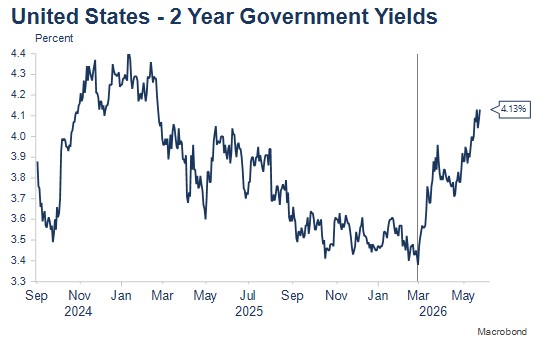

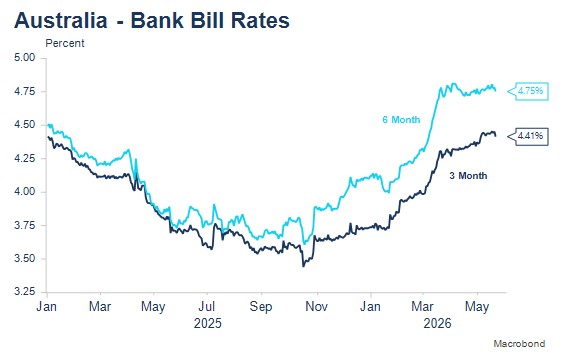

The repricing of the US short end continued over the past week, with US 2 year yields rising to a new cycle high of 4.13% and the markets now pricing one and a half US interest rate rises by April next year. This is quite a change - just a few weeks ago the US market was still considering and pricing a further drop in US interest rates was more likely, while the Australian markets had factored in one and a half more 25bps interest rate increases.

Policy and macro developments over the past week have supported the absolute and relative re-pricing.

First, the FOMC Minutes confirmed that many members of the FOMC supported a change in the wording of the interest rate bias to neutral. Furthermore, many members considered some firming of US monetary policy might be appropriate if inflation continued to run above target. This was more hawkish than revealed at outgoing Fed Chair Powell’s post FOMC press conference, where the focus was more on a change in the bias rather than discussion of possible tighter policy. My interest was also piqued in a number of references to IT-related inflationary pressures, independent of the Iran conflict.

Second, the RBA May Board Minutes strongly suggested the likelihood of a pause at the mid-June RBA Board Meeting, while Australian labour market data for April printed considerably weaker than expected by economists. Employment fell 19,000 against forecasts of a 15,000 increase, while the unemployment rate rose to 4.5% - an unchanged 4.3% outcome was forecast. More importantly, the 4.5% outcome was considerably higher than the RBA’s June quarter forecast average of 4.2%, released only two weeks ago, and not that far below the RBA’s forecast peak of 4.7% in two years’ time! That forecast had always looked odd given the extended period of below-trend growth anticipated by the RBA.

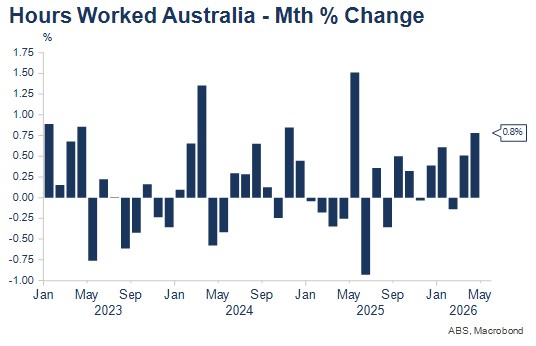

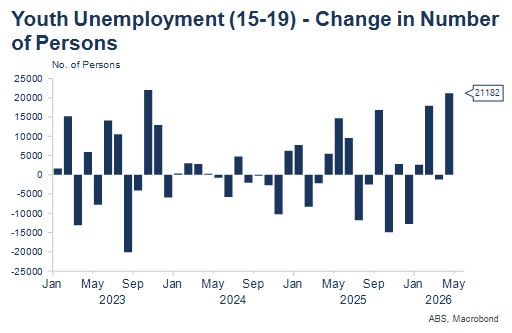

While the rally in Australian short-end markets clearly reflected overly bearish pricing and positioning, I would caution against over-interpreting the signal of the April labour market data. There were several contra-indications and non-confirmations in the data that should engender a healthy amount of distrust in the data. These included a further drop in the underemployment rate to 5.8% and a monthly surge in hours worked. The volatile youth unemployment category also accounted for a significant rise in the overall number of unemployed. I continue to suspect that the unusual calendar sequence of Easter, school holidays and the ANZAC Day public holiday in some states is more likely responsible for the outcome than a significant moderation in employment growth or rise in unemployment.

In the wake of the data, a number of economists that were holding onto the view of a rate rise in June against the RBA Minutes strong suggestion the three previous increases had created space for the Board to monitor developments in the Middle East and the economy for a time, pushed their forecasts out to August. At least one strategist declared Australia’s rate rise cycle over for this year. As a result, Australian markets now price just less than one further rate rise, with peak pricing by the February 2027 Board meeting (a further 25bps rate rise is now 95% priced). Emerging softness in Australian housing, likely accentuated by recent interest rate rises and budget tax change, have reinforced the more moderate outlook on market pricing.

The week ahead - key Australian and US events

It’s again a relatively quiet week data wise in the US, with the April PCE the key focus though around thirteen Fed speakers are also on the calendar. Australia has its monthly CPI data on Wednesday along with an evening speech from RBA Monetary Policy Board Member Carolyn Hewson in Adelaide. Australia also has the April Household Spending Indicator, which the Statistician is releasing a week earlier than normal to assist with assessment of the impact of the Middle East conflict on spending, while GDP partials are also released.

Markets look for a drop back in Australian headline CPI and Household Spending primarily reflecting the impact of Australian governments’ temporary fuel tax excise and GST relief. AIP figures suggest a 7% drop in petrol prices in April. More focus will be on analysis of the trimmed mean and in particular price changes for food, clothing and footwear, household furnishing and equipment and prices of newly constructed dwellings as this is where early signs of oil price pass through might be detected.

A 0.3% m/m core CPI would suggest that pass through had not yet accelerated, while a 0.4% (or higher) m/m outcome would point more clearly in the other direction. Either way, a peace deal is more important than this data for near-term market pricing.

Economists expect a 0.4% drop in Household Spending in April after a 1.6% rise in March. The latter primarily reflected higher fuel spending (both prices and volumes) as well as reported stockpiling of food. Government fuel relief should lower spending, as should some greater caution and less food purchasing, suggesting risk to the downside, albeit faster pass through would work in the opposite direction.

The RBNZ meets on Wednesday, with no change in interest rates widely expected. The key interest will be whether the interest rate track shifts earlier from the December rate rise previously indicated. SEEK NZ job ads remain consistent with only a slow improvement in the NZ labour market.

Wednesday 27 May: CPI (April); Construction Work Done (Q1); RBNZ OCR; Hewson Speech (6PM).

Thursday 28 May: Household Spending (April); Capex (Q1); (overnight) US PCE (April).

Outlook

My main concern in the past few months has been about a very extended closure to the Strait of Hormuz, as that would likely produce extremely high oil prices, recession and dislocations to economic activity. The diplomatic progress that seems to be occurring, including over the past weekend, suggests this major downside risk is receding. Should this prove to be the case, my expectation is that the world economy, after a period of oil market normalisation over some months, should be able to re-establish the pre-Iran conflict economic outlook.

That outlook was a more favourable one for US economic growth as the AI investment boom continued but also contained some inflationary pressures were emerging even ahead of the Iran conflict. These were evident in ISM prices paid and in comments and pricing suggesting potential shortages in semi-conductors and copper, as well as demand for power and water as data centres are rolled out globally.

To me, these pressures suggest US markets should not return to pricing interest rate cuts any time soon, with the next move in US interest rates more likely to be a rise. At the same time, the medium-term implications of AI for employment, inflation and interest rate policy in the 2+ years timeframe remain uncertain, with clear downside risks.

Australian interest rate markets as usual, are likely to take their directional cues from the US. Recent outperformance reflects some rare timing divergences between US and Australian monetary policy cycles and housing markets in Australia in recent weeks. There may be a little more of this to come, but the large move has likely occurred. I’d expect rate markets to rally in the near-term, unwinding some of the Iran conflict increase in yields if a peace agreement and Strait of Hormuz reopening occurs soon. But I’m inclined to be a medium-term seller after an expected shorter-term favourable move.