Perpetual Markets Economics and Interest Rate Commentary

RBA to increase interest rates 0.25% tomorrow. Oil prices continue to drive other investment markets (equities down, bond yields up). Sustained prices above $130-150pb would likely cause recession, while $230-300pb prices would be required to destroy 20% of oil demand in the short term.

Key points

- Major markets continue to follow the 1990 Gulf War playbook with spot oil continuing to rise, equity markets to weaken and bond yields higher as the Strait of Hormuz, through which 20% of global production ships daily, remains closed.

- It’s useful to analyse the current situation as the pre-existing economic scenario with a supply-side, oil price shock overlay. This is quite complex as the pre-existing situation included major short-term uncertainties about potential inflationary consequences of AI (the data centre rollout) as well as the potential longer-term deflationary consequences if significant job losses occur.

- The extent to which oil prices continue to rise depends critically on the length of time the Strait of Hormuz remains closed and the extent that energy producing infrastructure is destroyed in the conflict.

- I asked AI to summarise existing research to answer two key questions: (i) what level of oil prices would cause a global recession; and (ii) to what level do oil prices have to rise in the short-term, to temporarily “destroy” 20 million barrels of daily oil demand? My guesses were around $125pb and $180-200pb respectively. AI’s synthesis of IEA and IMF estimates were above $130-150pb and $230-300pb respectively!

- These are useful benchmarks – the implication for interest rate markets would likely be a tipping point somewhere above US$130pb, where the markets begin to factor recession risk into interest rate pricing.

- While conflict and associated oil price developments will continue to dominate market developments this week, there are also a host of central bank meetings (the RBA, Federal Reserve, ECB, BoE, BoC, SNB, Riksbank and BoJ). The commonality of communications on oil prices will likely provide important insight into how central banks might approach the crisis.

- In Australia, the markets are pricing around a 70% chance of a rate increase at Tuesday’s RBA meeting, This still seems a little under-priced on the basis of economic developments since February, the February forecast being predicated on the need for at least two rate rises being required to only very slowly return inflation to target, and Deputy Governor Hauser’s podcast appearance last week which strongly suggests the staff board paper position will be to recommend a further tightening to the MPB. Abstracting from Middle East developments, there was a clear case for tighter monetary policy, which Middle East developments do not yet invalidate.

- Elsewhere, the Fed is expected to leave interest rates unchanged, with most interest on the updated Summary of Economic Projections and Chair Powell’s press conference, where greater detail on the Fed’s thoughts and approach to higher oil prices may be revealed.

- In Australia, the main economic release is the February Labour Force Survey on Thursday. While the change in employment is often (appropriately) described as a random number, the unemployment rate tends to be a little less volatile. Recent readings have revealed the unemployment rate remains very low at around 4.1%, a level which is likely inconsistent with at-target inflation.

Qualitative construct for analysing current and prospective developments in economies and markets

Before commencing this week’s report, it’s worth laying out a framework for analysing and assessing current and future developments in the US and Australian economies and markets. The framework and approach have the following key aspects:

- It is mostly qualitative – I continue to be very sceptical about central bank or other organisation’s models’ ability to capture all the major forces impacting upon economies at the present time.

- The main construct is to think about the current situation as the base economic (and interest rate) scenario, with an Iran conflict/oil shock overlay.

The base or starting-point scenario we had been discussing had the following key elements:

- Low unemployment and above-target inflation in the US and Australia, though with inflation more above target in Australia than the US, and unemployment and the labour market tighter in Australia than in the US.

- Potential major economic impacts from AI. Importantly, there are two overlapping timeframes and divergent impacts to consider: (i) the potential for the very significant global data centre rollout to cause short-term inflationary impacts via capacity pressures in semi-conductors, selected metals (eg copper), water and energy; and (ii) the longer-term, potentially major, impact that AI might have on employment, particularly in white collar professions.

- Interest rates that are closer to neutral in Australia but still slightly restrictive in the US.

- A tariff shock that is impacting the US economy more significantly than the Australian economy, but where much of the adjustment to tariffs has likely already occurred.

In thinking about the Iran/oil shock overlay, the following key elements are relevant:

- The shock is another supply-shock, similar but importantly different to the supply chain difficulties experienced during the COVID pandemic. The similarity is that supply disruptions can reduce the availability of energy products (oil and LNG). Given the very inelastic nature of demand for energy, disruptions to energy supply impact on prices quickly, though different to COVID, higher energy prices also have a dampening effect on demand. Whereas during COVID, government stimulus and zero or near-zero interest rates added substantially to overall demand. In that shock, however, oil demand was substantially reduced due to lockdowns and reduced air travel. Interestingly, the RBA Governor recently noted that it is not helpful to have a supply shock when inflation is already above target!

- The key for the ultimate inflationary and economic consequences are not only how high oil prices rise, but how long they remain elevated, together with any actions central banks and/or governments take to lean against or ameliorate some of the effects.

The following conflict and oil price scenarios seem possible:

- Most bearish economically – the Strait of Hormuz, through which around 20% of global oil production (20 million barrels per day) flows, remains effectively closed for an extended period. The effect is even broader than oil with 20% of LNG shipments, and significant shares of global fertiliser and petrochemicals used in the production of plastics also shipped.

- Moderately bearish economically – the Strait of Hormuz reopens relatively quickly, but there is significant damage to oil infrastructure in the region.

- Most bullish economically – the conflict ends quickly and damage to oil infrastructure is very limited. Shipping starts flowing through the Strait of Hormuz in days or weeks rather than months.

Markets appear to be pricing some part of scenario 1, but without the ability to predict how long the shipping lane will ultimately remain closed, have not fully priced an extended closure.

Quantifying recession scenarios and the oil price required to “destroy” 20% of global consumption

I asked AI (CoPilot) what oil price would need to occur to produce a global recession. My intuition was that something above $125 per barrel on a sustained basis would pose significant risk. CoPilot returned the following relevant answers based on interrogation of various existing research and international agency modelling:

- It is not only the level and duration of high oil prices, but also the speed at which oil prices rise, that is important.

- Prices sustained above US$130-150 per barrel for one to two quarters would likely be sufficient to cause global recession based on previous episodes. Alternative quantifications include, when oil price expenditures exceed 5-6% of global GDP or when oil prices rise by 50-70% over a six-to-twelve-month period.

Based on existing analyses from the IMF and IEA, short-term oil prices around $230-300 per barrel would be required to temporarily “destroy” the approximately 20% of oil demand that is impacted by the closure of the Strait of Hormuz. That’s a little higher than my intuition, which was around $180-200 per barrel. The decision to release some 400m barrels from global strategic reserves negates the Strait’s closure for 20 days.

The week in review

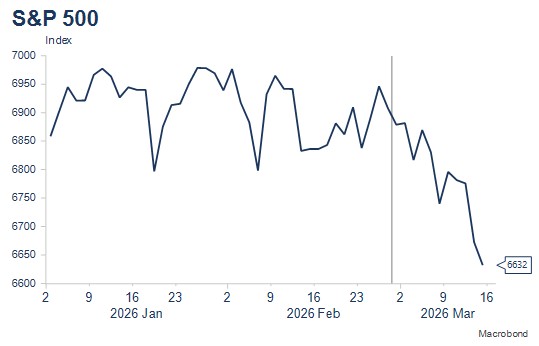

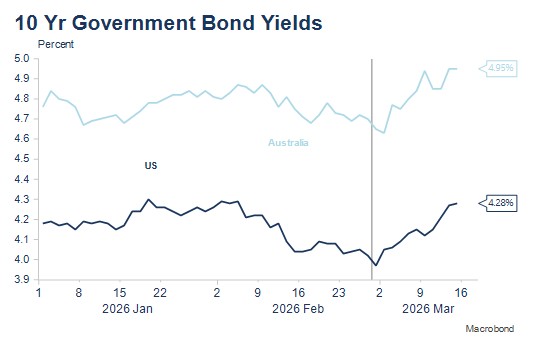

It was a slightly less volatile week, but the key trends we noted at the onset of hostilities remain in place. Oil prices have continued to rise but have yet to re-achieve the intra-day panic highs near $120pb of last Monday. Equity prices have continued to fall, while bond yields have also risen as markets price higher inflation in the near term. More substantial rises in oil prices will occur the longer the Strait of Hormuz remains closed, as will equity price declines, while a tipping point for bond yields and energy prices would likely occur somewhere above $125pb.

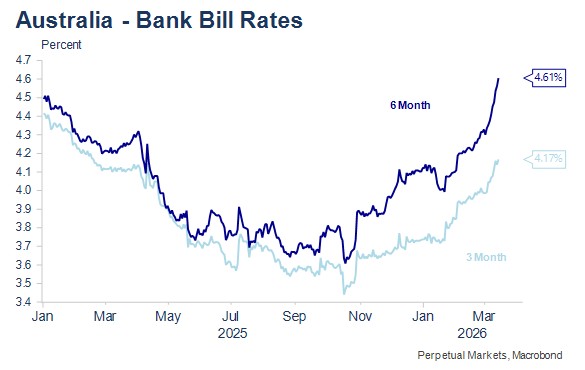

Short-term interest rate markets have been interesting. Market pricing for US interest rate cuts has been reduced and pushed further out, while in Australia, the reverse has occurred, with interest rate rise timing brought forward and increased. At the end of last week, the US market was pricing a full rate cut only by March 2027, compared to previous week’s pricing of two rate cuts by July this year. In Australia, where the market previously discounted two rate increases by November this year, there are now nearly three rate increases priced this year, with the next rate rise fully priced for May. This saw a 20 basis point increase in 6-month bill yields over the past week, but even then, the probability of a move at this week’s March Board meeting of around 70% seems a little under-priced.

The RBA Board’s decision in March

Arguments for a 0.25% increase in interest rates.

The RBA staff’s February forecast update was predicated on two 0.25% increases in the cash rate this year, the first of which was delivered in February. Even with two increases, the forecasts anticipated a very slow return of inflation to target, only by mid-2028. Given the extended period of high and above-target inflation already experienced and the risk of the de-anchoring of inflationary expectations, the Board is likely to want to move interest rates relatively quickly to a level that will return inflation to target.

Since the February board meeting:

- The unemployment rate has remained at 4.1%, a level the Bank continues to signal represents a labour market that is a little tight.

- December quarter GDP printed more strongly than expected both on a quarterly and annual basis. This means there are even more capacity pressures than when the RBA staff forecast in February that two interest rate increases would be sufficient to return inflation to target.

- Trimmed mean inflation printed at 0.3% m/m and 3.4% y/y, rates that mark a material departure from the 2.5% midpoint of the RBA’s inflation target.

- Oil prices have risen very markedly, rising over $30 a barrel or around 43%. While the ultimate impacts on the economy and inflation depend importantly on both how high prices rise and for how long prices remain elevated, a supply driven oil shock such as this in an already above-target inflation world, creates additional risk that inflation expectations could de-anchor, even though there is an associated negative demand effect from higher oil prices.

- RBA Deputy Governor Hauser appeared in an unusually timed podcast, released the day before the pre-board communications blackout commenced. The podcast contained wide ranging discussion of monetary policy and inflation and is unusual so close to a Board meeting. This strongly suggests the Board paper prepared by the RBA staff will recommend a tightening to the Monetary Policy Board.

In addition:

- Moving again in March would allow the Board the chance to pause in May, avoiding being drawn into fiscal policy debates with the media and allowing consideration for the impact on the economy of mooted spending cuts in the May Budget.

- Former RBA Governor Ian Macfarlane believed the best approach when interest rates were at the wrong level was to move them to the perceived “correct” new level relatively quickly. This has frequently led to back-to-back moves at the start of new easing or tightening cycles.

Arguments against tightening monetary policy:

- High oil prices and the uncertain situation in the Middle East create too much uncertainty with significant risk that a tightening could very quickly be shown to have been unwise (this argument can be fairly easily countered by acknowledging the Board could quickly reverse any tightening move if it became shown to be unnecessary).

- Financial conditions have tightened due to lower share prices, higher bond yields, higher oil prices and a higher $A.

Together, the above suggest the Board could simply wait a further six weeks to see how the Middle East situation develops.

On balance, I feel the Board will relatively easily conclude that the arguments for further tightening of policy at this meeting are strong and delaying such a decision risks de-anchoring inflation expectations, notwithstanding the additional uncertainties created by the conflict in the Middle East. Effectively, the domestic economic and inflation fundamentals already justify at least one further near-term tightening and Middle East developments have not yet rendered that conclusion invalid.

The week ahead: Economic Calendar – Key Australian and US events

Monday 16 March – (overnight) US Industrial Production (I’m interested in the capacity utilisation reading).

Tuesday 17 March – RBA Board Meeting (25bps increase in the cash rate expected by Marex).

Wednesday 18 March – FOMC meeting (overnight). No change in interest rates expected by Marex (and the markets). Focus will be on the Powell press conference and the extent to which current oil price rises constitute a new inflationary challenge. RBA releases half-yearly Financial Stability Report.

Thursday 19 March – Australian Labour Force, February. (Employment median forecast of +20K (previous +18K); Unemployment 4.1% expected (previous 4.1%). This is the most unpredictable of Australian economic indicators. The unemployment rate is the key – at 4.1%, the RBA has continually characterised the labour market as a little tight, a description that is meant to convey an unemployment rate that is below the level consistent with at-target inflation, without suggesting the RBA wants to see higher unemployment.

There are also numerous other central bank meetings (BoC – Wednesday; ECB, BoE, SNB and Riksbank – Thursday) and BoJ (Friday). With no policy rate changes expected, it will be interesting to contrast the communications each bank makes in relation to the current oil price rise and the implications for monetary policy.